America's Income Crisis: How It's Triggering a Collapse in Birth Rates

The real reason the average American is so downbeat about the economy.

There’s been a growing debate in financial media about why consumer confidence remains so weak despite what appears to be a prosperous situation on the surface, such as the monthly job numbers or the dramatic increase in the stock market.

Numerous articles in Bloomberg and the Economist have tried to tackle why consumer confidence has diverged from its long-standing relationship with the stock market.

The reality is that real income has fallen sharply from the pre-pandemic trendline, and this has caused the average American to feel as though they are far behind where they expected to be several years ago.

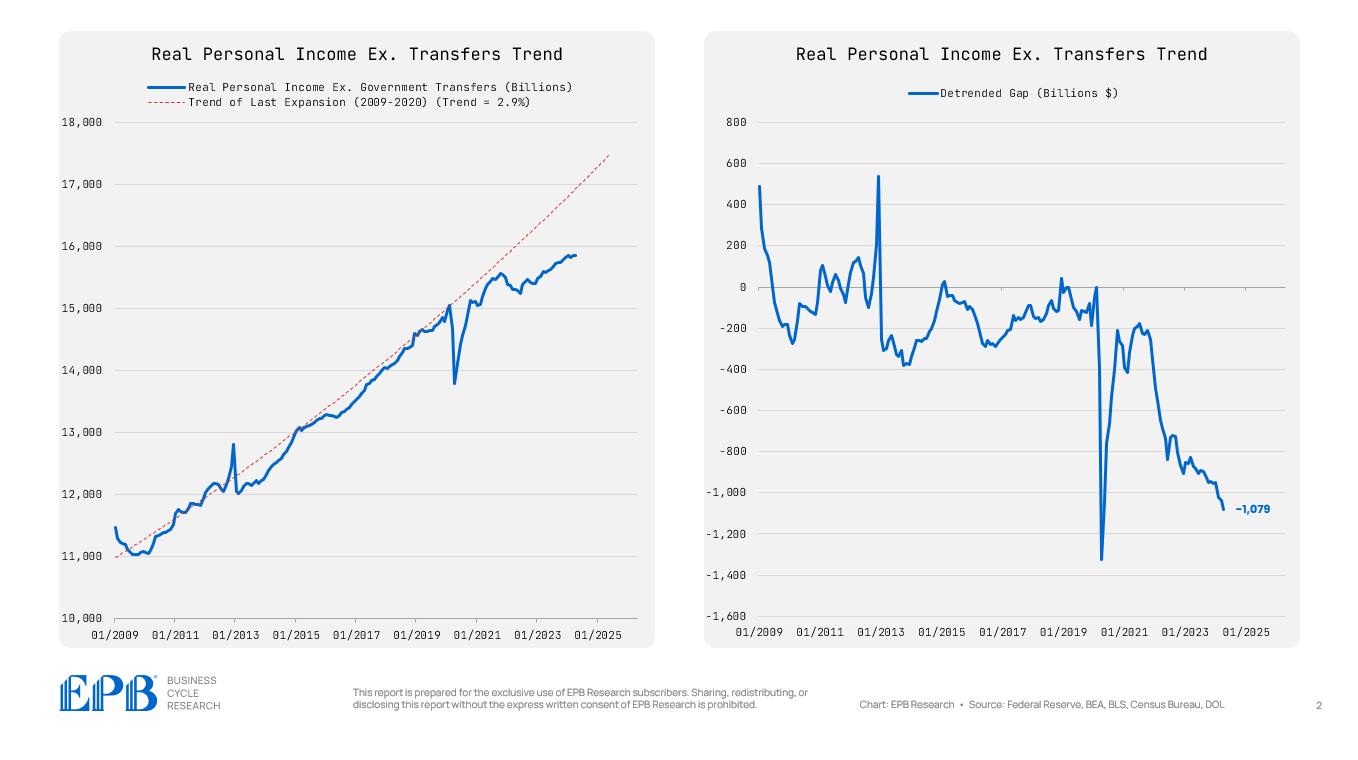

The following chart shows real personal income excluding government transfer payments. This means all income, including wages, interest income, rental income, dividend income, and more, all adjusted for inflation.

The only income that is excluded is income from the government, and it’s excluded for a specific reason. We are trying to capture the private sector's ability to generate real income. Secondly, there is a concept in economics called permanent income or long-run income.

Income that comes from the government is generated through taxes or deficits, and it is not perceived as a long-term, sustainable source of income. The COVID stimulus payments, supercharged unemployment benefits, and PPP loans were generally used for short-term consumption, not savings and economic investment, which in turn generates a more sustainable income stream.

For these reasons, the most important metric for understanding consumer confidence is the private sector's ability to generate a long-term, reliable stream of real income.

From the end of the 2008 recession to the start of the COVID recession, real private sector income increased at a consistent 2.9% pace. The average American, in 2018 and 2019, had a perception of roughly where they’d be in 2023 and 2024 – this is the concept of long-run or permanent income. After the pandemic, real private income is materially short of that pre-pandemic trendline.

These two charts show the same concept. The chart on the left is the exact same graph, real private sector income against the pre-pandemic trendline and the chart on the right is the gap between the red trendline and the blue line of actual real private income.

You can see in the right-hand chart that real private income bounced around the zero-line which means real private income was hovering around the trendline. After the pandemic, a widening gap emerged to the point where today, real private income is over $1 trillion less than where it was projected to be based on the pre-pandemic economy.

Of course, the government tried to plug some of this hole with heavy transfer payments, and that helped in the very short-run in 2020 and 2021, but part of the reason that the gap is widening today is because those transfer payments created a burst of inflation, and then the payments ended, and now consumers are back to their original, primary sources of income that did not keep pace with total inflation.

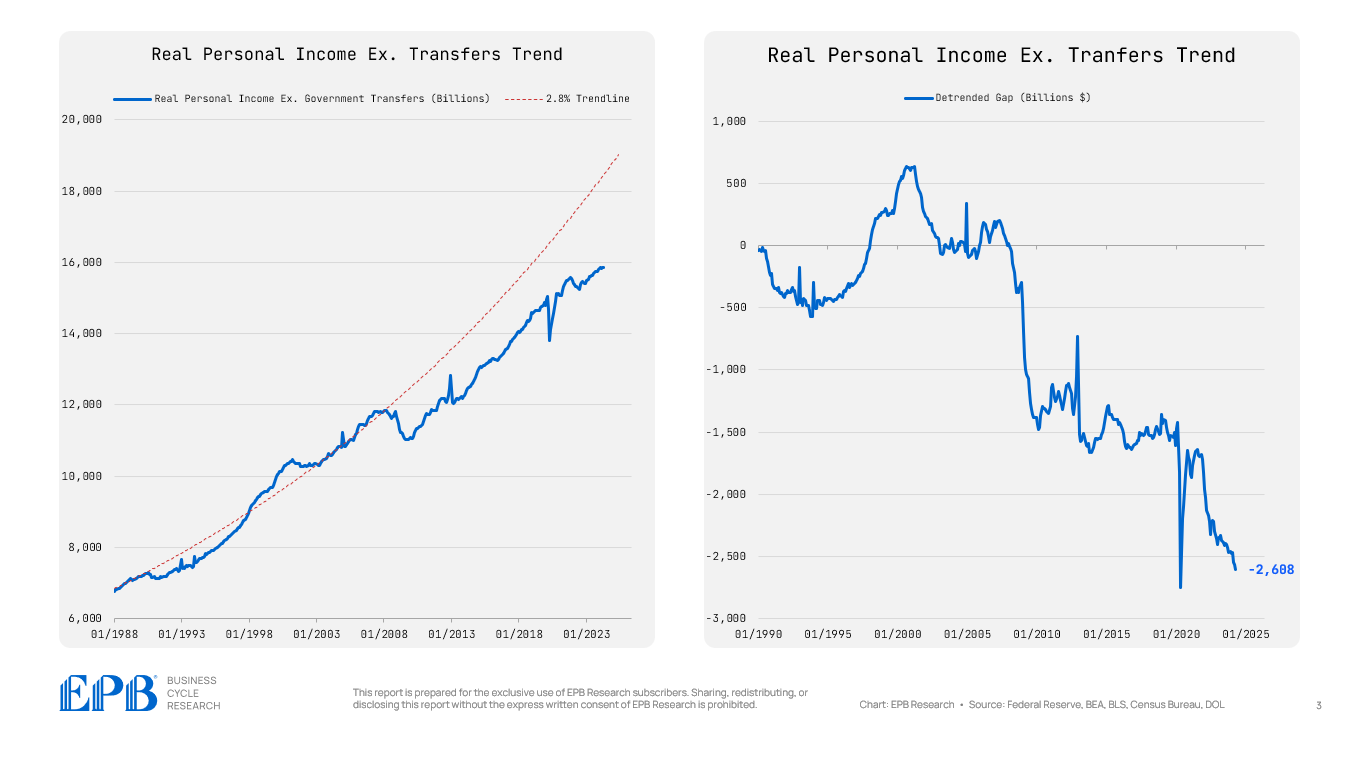

An even more startling reality is that if we draw a similar 2.8% trendline for real private income, we can see that the economy generated a very consistent pace of private income from 1988 to the start of 2008 – a 20-year stretch of consistent income gains. Of course, there is volatility around the trendline, but over the longer run, real income gains were strong and stable. The chart on the right shows the gap between the 20-year red trendline and actual real private income. You can see that the gap was negative after the 1990 recession, then increased during the economic recovery, and then collapsed after 2008, never to recover back to that trendline. Private sector real income is now $2.6 trillion lower than it would have been if the economy maintained that 2.8% trendline that it was able to produce for the 20 years from 1988 to 2008. This 2008 breaking point will come up again at the end of this article.

Now, you might say 20 years is not that long. Well, we can pull that same 2.8% trendline back to 1966!

The economy maintained a long-term real private income trendline of 2.8% from 1966 until 2008, and then it broke. It broke once more after the pandemic.

This is why consumers are feeling so downbeat about the economy despite the gains in the stock market. The average American continues to fall short of there they expected to be 5 years and 10 years in the future.

What’s happening is that as the economy becomes increasingly indebted, both at the private level and the public government level, the ability of the private sector to rebound from shocks and recession is impaired.

In the past, we’d have a recession, real income gains would drop but then recover in the next expansion.

Now, each time there is a recession or a shock, the private sector fails to regain the prior trendline in terms of the ability to generate real income, and the consumer is left with a feeling of falling further and further behind – this is the true situation facing most Americans that don’t have large stock portfolios to offset the reality of a weaker and weaker private sector.

If we look at real private sector income per capita on a 20-year average basis, we can see that in the 1970s, Americans had a 20-year stretch where the average person was experiencing real income gains of 2.5% to 2.8%.

Over the years, these income gains have become weaker and weaker. Today, the average American has experienced real private sector income gains of 1.8% over the last twenty years.

Of course, this is just an average. Some Americans are far above this 1.8% level, which means many Americans have seen real income gains from private-sector sources of 1% or less for 20 years.

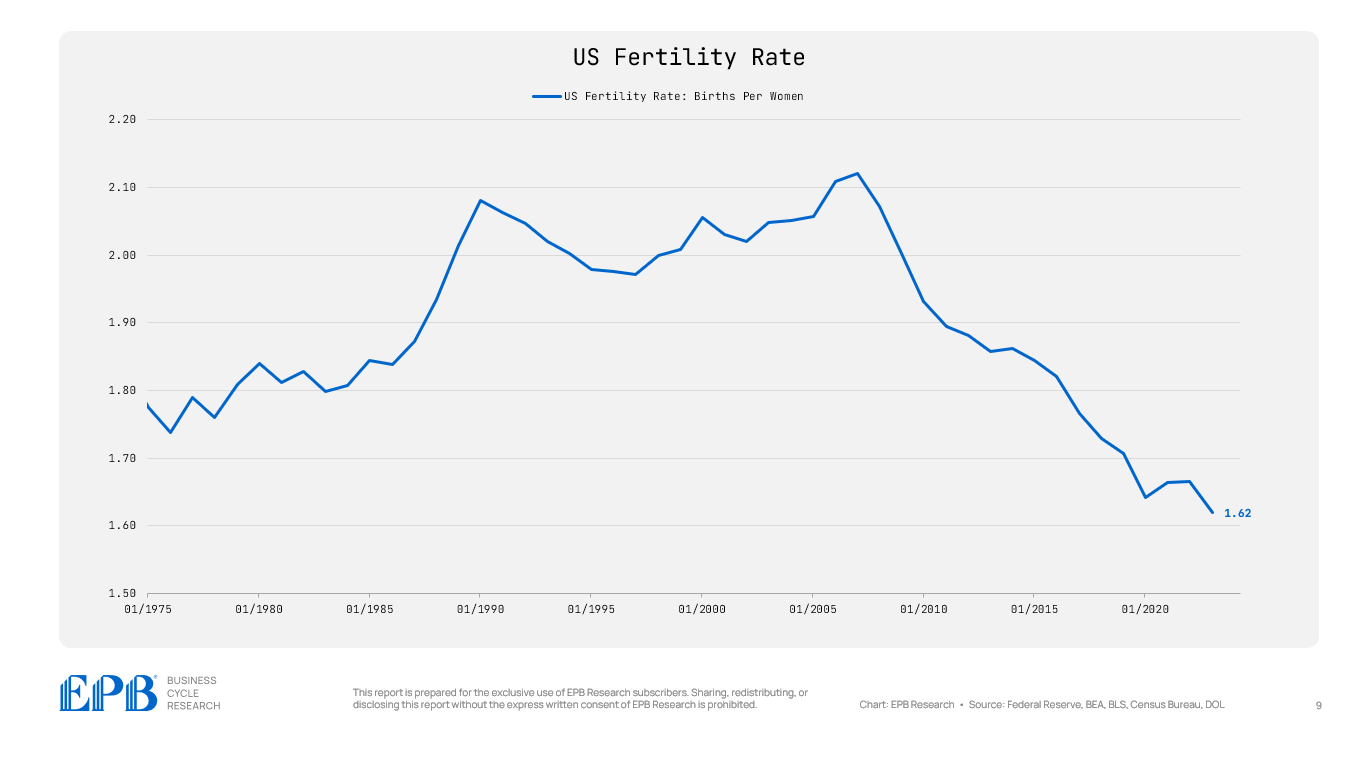

This slow but consistent deterioration of the private sector’s ability to generate strong income gains has led to a collapse in birth rates. The birth rate is the ultimate consumer confidence barometer. If you are confident about your income and your future, household formation is a natural goal.

However, if you feel you are falling behind and finding it harder and harder to move ahead without dependents, the idea of starting a family and taking on more financial burdens is less appealing.

This chart shows the fertility rate or the average number of births per woman in the United States back to 1960.

In 1960, the average woman had 3.5 births and that number fell sharply through 1975 as women entered the workforce. This was a structural shift in the economy so we should look at the birth rate after this shift occurred.

From 1975 through 2008, the fertility rate in the US increased as the private sector generated strong and stable real income gains for the average American.

Recall that 2008 breaking point from our earlier real income charts.

Starting in 2008, the fertility rate collapsed and it has been moving lower almost every year in the same exact fashion as the real income gap from our prior charts.

The fertility rate has dropped to a record low in the United States of just 1.6, which is far below the replacement rate.

Sure, the stock market continues to rise, but there should be no mystery as to why the Average American continues to feel increasingly downbeat about their economic prospects and expresses that feeling through a lower birth rate.

This lower birth rate, while a longer-term issue, becomes self-reinforcing as economies struggle with declining population levels, but that is the topic for another article.

If you enjoyed this post and want to learn more about the EPB Business Cycle Framework or our composite indexes, check out our Free 5-Part Business Cycle Traning Series.

The debt/GDP is killing the American dream. It's a smokescreen for the greatest transfer of wealth and creation of income inequality. People need to wake up, our children's economic futures are being diminished.

Numbers don’t lie. It’s pretty obvious what Fed and Wall Street are doing…Jamie Dimon said it best… “happy talk”. When reality hits populous the slide will start slowly, then…Eric, excellent presentation of reality.