Residential Construction Backlogs - How Much Longer?

Measuring the existing backlogs in the residential construction sector and analyzing the future impact on employment within this critical industry.

The residential construction sector is arguably the most critical component of the US economy. Despite its relatively small size, it is responsible for a large portion of the recessionary ebbs and flows.

Popular papers such as Ed Leamer’s “Housing Is the Business Cycle” have examined the residential sector's importance to GDP, inflation, employment, and Fed policy.

The residential construction sector is a high multiplier, interest-rate sensitive, and capital-intensive sector that is hyper-responsive to changes in monetary policy.

In 2022, 2023, and 2024, the residential construction sector continually surprised in its strength despite a historically large monetary tightening cycle. The reason for this uncommon strength is the construction backlogs accumulated in 2021 and 2022, which rendered one of the most interest rate-sensitive sectors of the economy insensitive to monetary policy while the backlogs cleared.

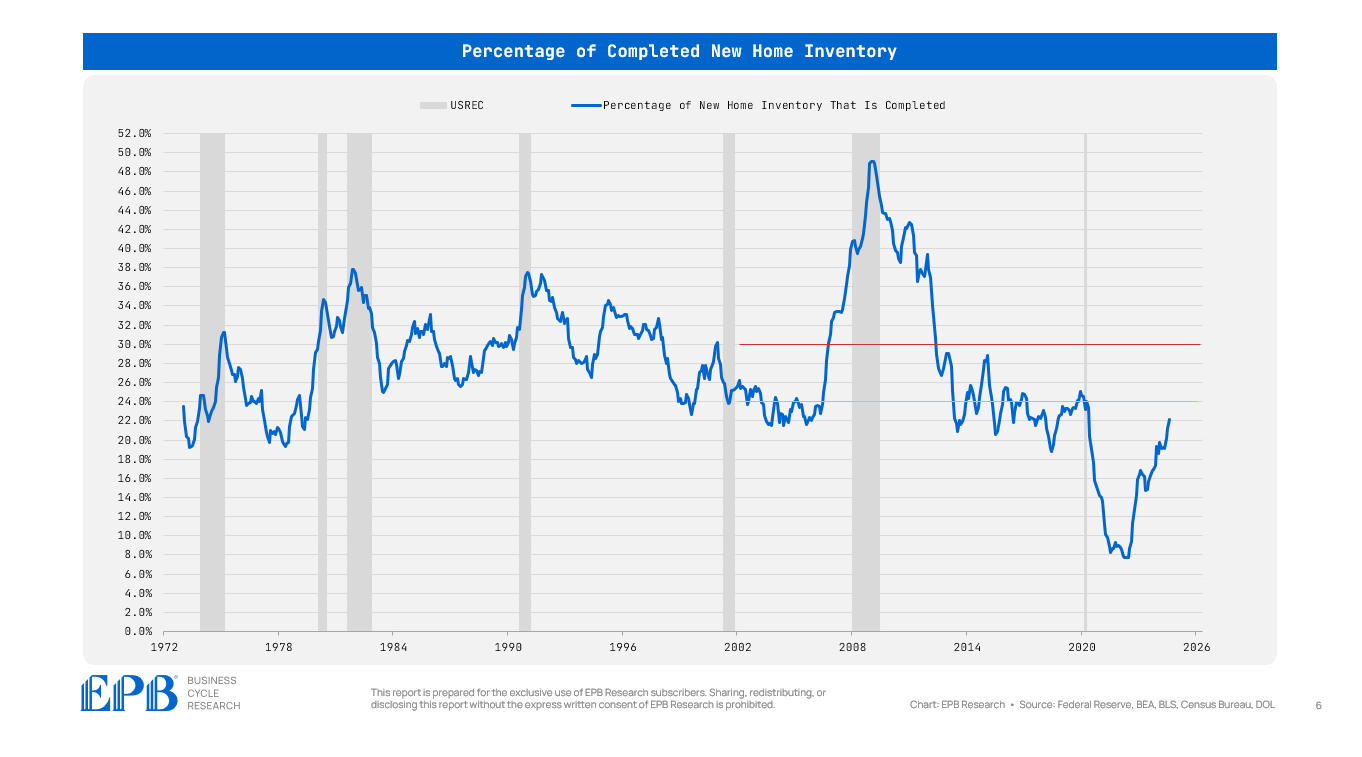

To illustrate, the chart below shows the percentage of new home inventory that is completed.

Homebuilding companies can offer inventory for sale that is completed, under construction, or not yet started. Usually, about 20% to 30% of new home inventory is completed, while 70% to 80% is under construction or not started.

In 2022, demand was so elevated while supply was constrained that 8% of new home inventory was completed.

In other words, 92% of new home inventory was under construction or not started yet.

The Federal Reserve could have raised rates to 10% at that time, but homes were already financed and purchased, and they needed to be built regardless of future interest rates.

This was the most significant distortion ever recorded in the new construction market.

Here we sit two years later, and 22% of new home inventory is completed, still below the 25-year historical norm of 24%.

In recent months, the percentage of completed inventory has increased slightly less than 1% per month.

If we continue at this current pace, the percentage of completed new home inventory will rise to the historically normal 24% level in 2-3 months and increase beyond the 30% level in 8-9 months.

The 30% level and above is more consistent with sharp residential construction job losses, while the 24% level is representative of the pre-COVID norms.

There are many variables at work, so these historical limits are not firm rules regarding when homebuilders will suddenly shed labor, but they are general ranges that can highlight whether the ever-important residential sector is in a state of backlog or overproduction.

Recessionary job losses are always most concentrated in construction and manufacturing. We can narrow this further to residential construction and durable goods manufacturing.

The collective of these two sectors must always experience sharp job losses around recessionary periods. Sometimes, both sectors contribute to job losses, and sometimes, one sector suffers more significantly.

Due to backlogs, residential construction is still adding jobs, while the durables manufacturing sector is starting to shed jobs more aggressively.

The chart below shows the 3-month average change in employment for the combination of residential building and durables manufacturing.

The chart highlights the -20k to -40k range as the proximate recessionary zone.

Currently, the two sectors are averaging job losses of 5k to 10k, a significant factor contributing to the weakening labor market trends but not substantial enough to spark a recessionary spiral.

Backlogs in the residential construction sector still exist and will remain for another 2-3 months before reaching a historically average level of completed inventory. Job gains in the sector will become more difficult at that point, and sharp job losses are a high risk in 6-8 months if current trends persist and push completed inventory north of 30%.

In the meantime, the durables manufacturing sector is shedding jobs, and an increased pace of job losses from here risks the recessionary warning zone, even without negative contributions from residential construction.

Watching the trends in residential construction and durables manufacturing employment is vital to navigating the Business Cycle and future recessionary risk.

Before you go, please enter your email below to avoid missing a future update!

Feel free share this post with anyone you think would find it valuable.

Great work

Great analysis, as usual!